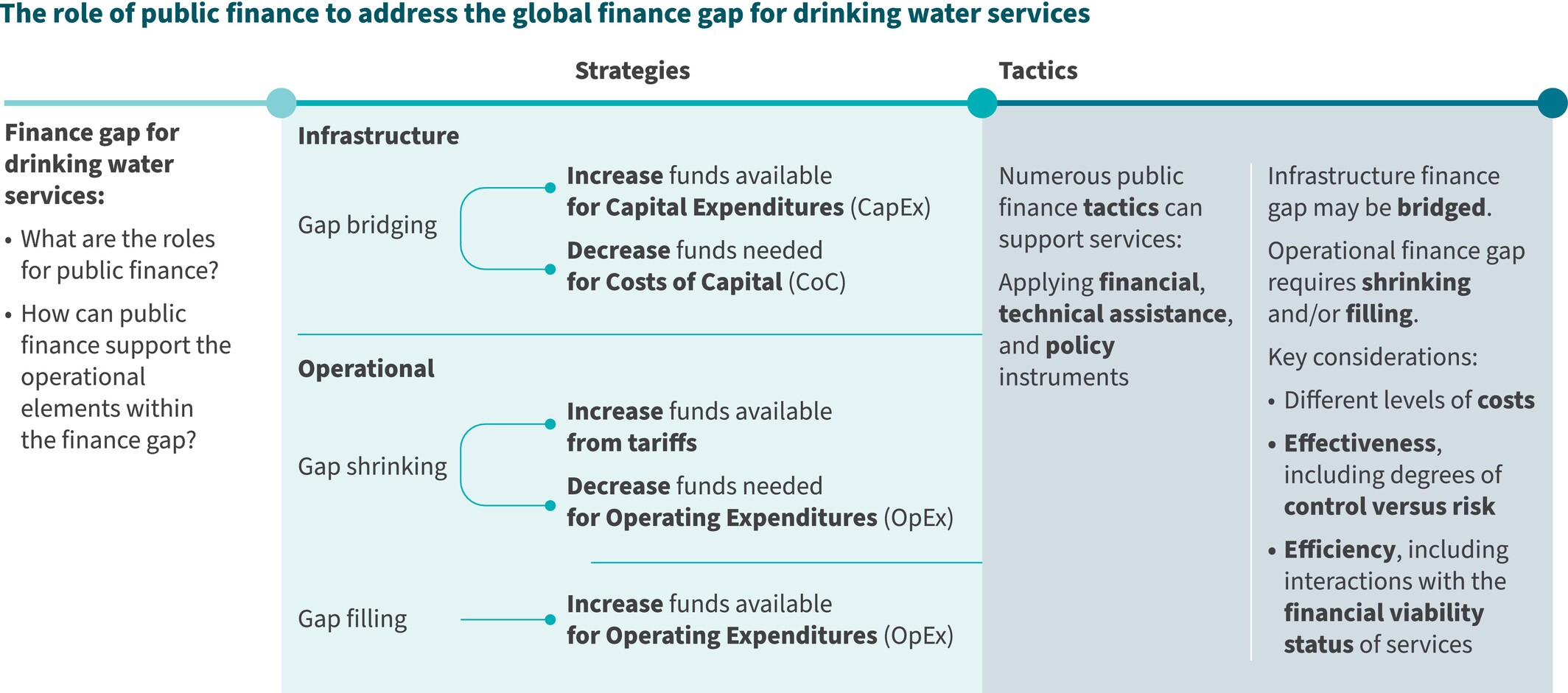

There is a multibillion-dollar finance gap slowing progress towards universal drinking water services. Focusing on how governments are investing to address this gap, a new open access research article examines the different elements that contribute to this gap, and argues that the funds needed for operations & maintenance (O&M) of services should be considered differently from the funds needed for infrastructure. With the functionality and sustainability issues the sector faces, these differences are worth paying attention to.

This research suggests a framework of five strategies for bridging, shrinking, and filling the finance gap for drinking water services, based on how the funds available from tariffs, taxes, and transfers compare to the life-cycle costs of services.

A framework for bridging, shrinking, and filling the finance gap for drinking water services (Nilsson, 2025)

Do we need a new framework?

Maybe, yes! Approaches for targeting gaps in infrastructure finance have been well studied, with many frameworks already available to guide actions and suggest new funding sources and mechanisms. However, the parts of the finance gap related to operational needs has been less analysed, even though there is an increasingneed foroperationalfinance.

The water sector continues to struggle with the financial sustainability of drinking water services. Most repayable finance sources are not suitable for operational costs, and so it falls to governments and service providers to see how to balance ongoing costs and revenues. This framework shows that, after construction, there are fairly limited options: increase tariffs, cut costs, and/or set up subsidies.

How can the operational finance gap be addressed, to keep water services flowing?

This research studied 213 examples of government investments for drinking water services, from 68 countries, to see how public finance is being used to address the operational finance gap. It found 13 tactics being used by governments from around the world, using financial, technical assistance, and/or policies, to:

increase funds available from tariffs, and/or

decrease funds needed for operations & maintenance, and/or

increase funds available for operations & maintenance through subsidies.

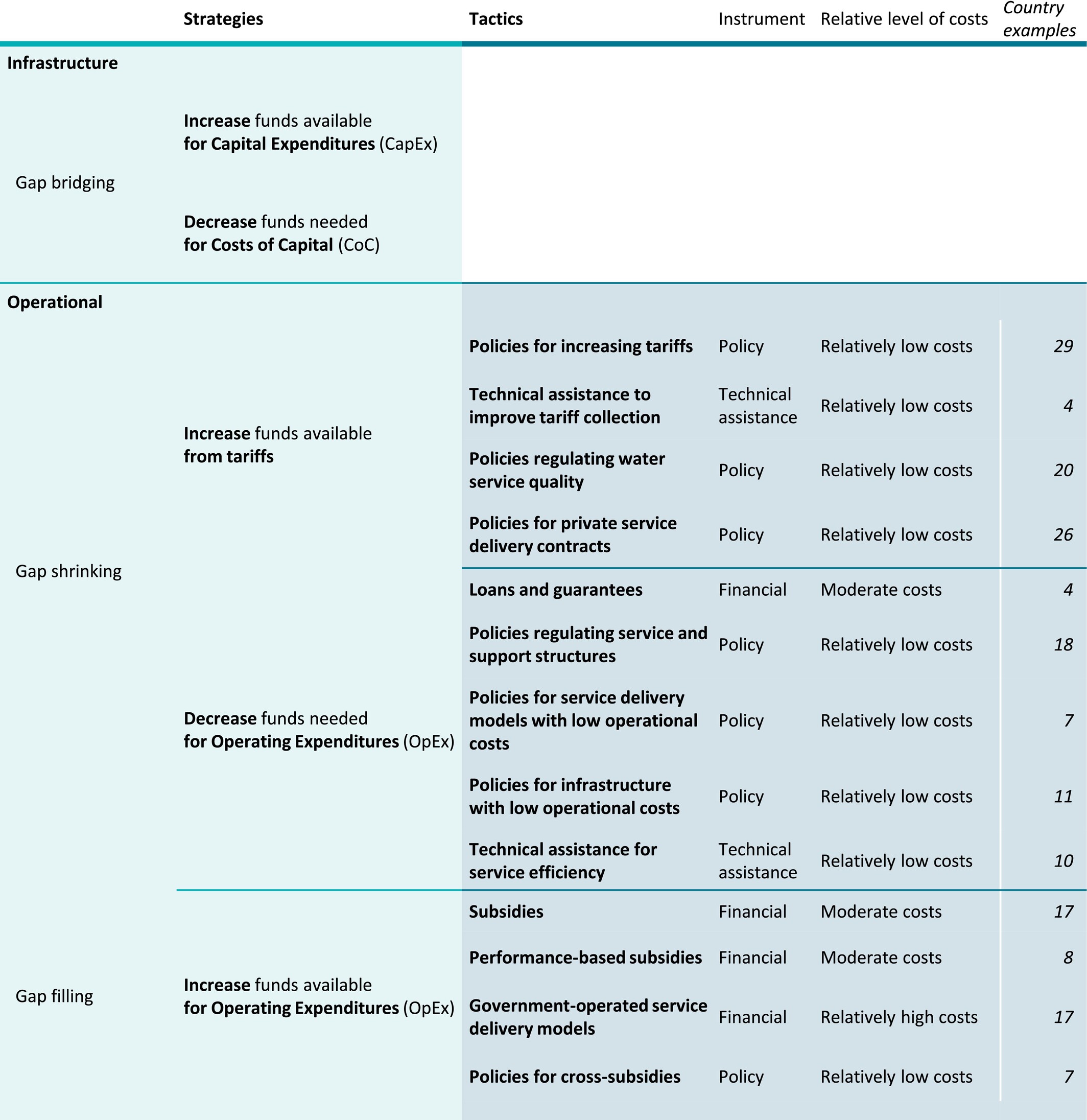

These tactics, and their investment requirements, are presented here:

Public finance tactics to support operations of drinking water services (Nilsson, 2025)

Which tactics are being applied in your areas, by governments, or by other sector actors? Which are not?

Are the tactics being used achieving what is needed, supporting services for more people, and services which are more financially sustainable?

Are there other tactics being used that are not captured here?

About the author: Kristina Nilsson is a governance and development professional with over a decade of experience working on water and sanitation service delivery in Africa and Asia. She is currently a PhD student at the University of Oxford, researching public finance support for rural drinking water services.

Rural water supply systems in low-income settings, particularly in last-mile communities, face chronic sustainability challenges. Financing predictable operation and maintenance (OPEX) remains a persistent gap, with one in four water points in sub-Saharan Africa being non-functional at any given time. While community-based management has been the dominant model for post-construction maintenance, it is increasingly recognized as insufficient, relying on underfunded household tariffs, volunteer committees, and limited technical support. Emerging solutions like results-based financing and professionalized maintenance contracts have shown promise with some securing government financing. This paper proposes district-level maintenance endowment funds, a mechanism where invested capital generates predictable income, as another option for financing rural water maintenance. These funds would support targeted subsidies, results-based contracting, and accountable, locally governed service delivery aligned with decentralization frameworks. This proposed model is agnostic to the specific management model, whether community-based, professionalized, or hybrid. The focus is on creating a predictable, long-term financing mechanism, particularly for so‑called ‘last-mile’ rural communities: small, dispersed villages, often with fewer than 1,000 people, that are typically excluded from piped water systems due to high per-capita service costs.

Two key arguments frame this proposal: (1) while endowment funds may be initially capitalized by international donors or organizations, over time they reduce dependency on short-term donor cycles by creating a predictable, locally managed revenue stream, and (2) Piloting endowments at the district government level strikes the right balance between being close enough to last-mile communities, accountable to them, and large enough to achieve economies of scale that will ensure financial viability for service provider payments.

THE PROBLEM: Persistent Non-Functionality and Unrealistic Expectations

Across sub-Saharan Africa, one in four rural water systems are non-functional at any given time. These failures are not anomalies, but they reflect a systemic global challenge: the absence of a reliable model for rural water service delivery beyond construction. For decades, community-based management (CBM) has been the dominant approach. It assumes that because communities value water, they will voluntarily manage infrastructure. But the viability of CBM is increasingly being questioned. Tariffs based on affordability rarely cover full maintenance costs, especially in small, dispersed communities, with variable incomes, that are often not prioritized for piped systems. Trained committee members often leave, and access to spare parts or technical support is limited. Volunteer fatigue, lack of retraining, and systemic underinvestment compound the problem.

The expectation that people living in the poorest rural villages must fully fund and manage the long-term maintenance of their own water systems does not align with how water systems are managed anywhere else in the world. In high-income countries, water infrastructure is maintained by trained professionals and supported by stable funding streams, often not limited to water user fees, but supplemented by public financing mechanisms such as property taxes and municipal budgets. The same should hold true, if not more so, in low-resource rural settings. A more realistic, equitable approach is therefore urgently needed.

TRIED AND TESTED SOLUTIONS: Results-Based Financing (RBF) – When Performance Meets Poverty

New RBF models are emerging. Uptime, as an example, is a partnership supporting professionalized rural water service providers that pays providers based on verified uptime. This shifts incentives from reactive repairs to preventive maintenance. Between 2020 and 2022, Uptime supported services for 1.5 million people in seven countries. Governments in countries such as Kenya, Bangladesh, and Zambia are now beginning to adopt performance-based financing approaches like this into their own public financing systems. This has been inspired in part by the evidence generated through philanthropic pilots. Yet, a central limitation remains: these models have demonstrated viability primarily in communities large enough or more “well-off” to generate economies of scale. This makes them financially attractive to service providers, but systematically excludes smaller, remote last-mile communities that are seen as less “bankable”. This is not a critique of performance-based models like Uptime, they are delivering results and proving their value. But it does highlight the need to pilot complementary result-based financing mechanisms that can address the unique realities of last-mile communities. Expecting the world’s poorest to fully finance their own essential services is neither equitable nor realistic. What’s needed is smart, targeted financing, including well-placed subsidies, that reflects the diversity of community capacity and directs public investment where it’s needed most. This is especially critical for last‑mile communities, i.e. remote, low‑density villages where user fees alone can never sustainably cover operating expenses.

This frame of thought, of differential and context-specific financing solutions, borrows from Dorward et al.: “Hanging In, Stepping Up, and Stepping Out.” Most rural households are “Hanging In,” unable to pay without full subsidy. Others can co-finance with support (“Stepping Up”), or engage with market models (“Stepping Out”). This model enables differentiated financing that aligns with real-world capacity. Targeted subsidies are not about dependence; they free up cash for productive use while ensuring reliable services. Importantly, we differentiate between water as a service that must be reliably provided for health and dignity, and water as a productive resource used to generate income. The proposed endowment-backed financing model speaks to the former, guaranteeing essential domestic supply. Other financing tools may be more appropriate for supporting productive uses of water in agriculture or enterprise.

RBF models have proven we know how to make maintenance work. The challenge now is to pilot solutions, such as endowment funds, that can sustainably support these communities where market-based approaches do not reach, thereby ensuring universal access to all.

THE PROPOSAL: District-Level Maintenance Endowment Funds

To close the financing gap, we propose district-managed endowment funds dedicated to rural water maintenance. These funds would invest capital to generate steady income for maintenance costs, insulating service delivery from budget shocks and donor cycles. They would:

Provide predictable financing by requiring implementing agencies to allocate a fixed amount, e.g. 10-20% of infrastructure costs, into the fund.

Enable targeted subsidies using the Hanging In/Stepping Out framework.

Support results-based contracting for professional maintenance providers.

Align with decentralization by placing fund management at the district level, while national governments serve as regulators.

This model borrows from urban utility principles where professional service delivery is underpinned by predictable financing and adapts them to rural realities. It does not assume full cost-recovery from users, nor does it treat water as a commodity for profit. Instead, it creates a stable platform for targeted subsidies and professional maintenance services in communities where user fees alone are structurally insufficient.

This blog post is part of a series that summarizes the REAL-Water report, “Financial Innovations for Rural Water Supply in Low-Resource Settings,” which was developed by The Aquaya Institute and REAL-Water consortium members with support from the United States Agency for International Development (USAID). The report specifically focuses on identifying innovative financing mechanisms to tackle the significant challenge of providing safe and sustainable water supply in low-resource rural communities. These communities are characterized by smaller populations, dispersed settlements, and economic disadvantages, which create obstacles for cost recovery and hinder the realization of economies of scale.

Financial innovations have emerged as viable solutions to improve access to water supply services in low-resource settings. The REAL-Water report identifies seven financing or funding concepts that have the potential to address water supply challenges in rural communities:

Village Savings for Water

Digital Financial Services

Water Quality Assurance Funds

Performance-Based Funding

Development Impact Bonds

Standardized Life-Cycle Costing

Blending Public/Private Finance

Understanding Blended Public/Private Finance.

Water supply development in low- and middle-income countries has traditionally relied on public or aid funding, rather than commercial financing. “Blended” finance refers to leveraging public funds (e.g., concessional loans or grants from national governments or development banks) to mobilize additional capital from private banks or investment groups (OECD 2019b).

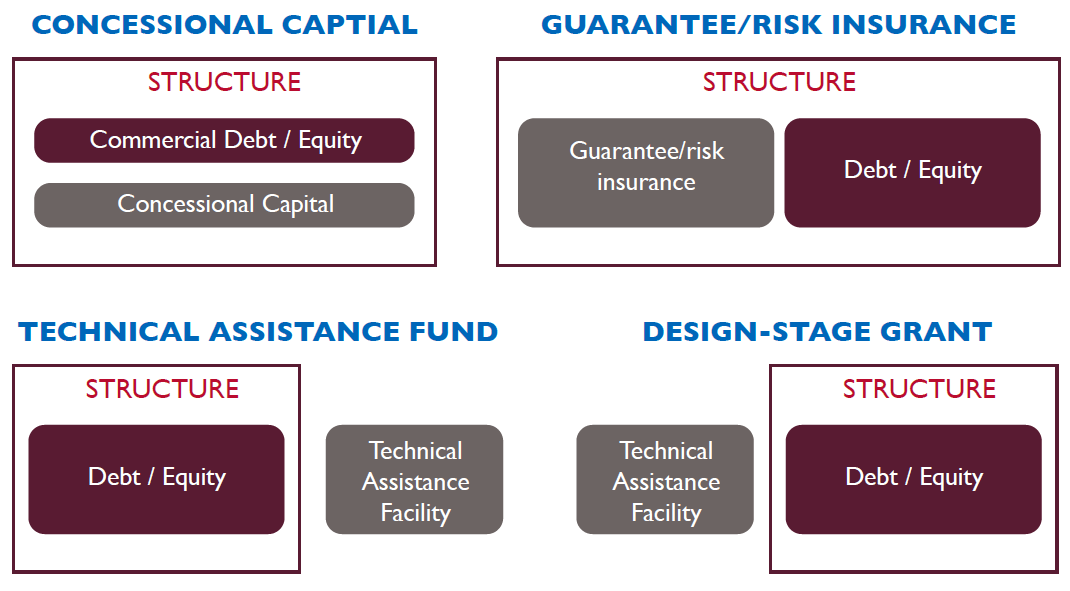

Combining development finance with private investment can assume different structures to reduce risk, employing a range of instruments (e.g., equity, debt, partnerships, technical assistance, grant-funded transaction design, guarantees, or insurance; Figure 1; OECD 2019a; Convergence 2023). The most common blended finance instruments across the development sector from 2018–2019 were direct investments in companies or subsidiaries, loan guarantees, “syndicated” loans, and lines of credit (OECD 2019a). Syndicated loans come from a group of collaborating financial institutions (a loan syndicate) to a single borrower, reducing the risk and buy-in amount needed for each individual group and/or ensuring sufficient specialized expertise. Alternatively, a smaller amount of pure grant funding may be used to support technical assistance or subsidies, with the goal of attracting other investors.

Figure 1. The four most common blended finance structures (adapted from Convergence 2023)

Examples

Although not all water-related “public-private partnerships” leverage public funding to attract commercial finance, these long-term collaborative arrangements among one or more government and private sector entities have been in place for decades in low- and middle-income countries, including throughout Africa, with encouraging results. Overall,

private operators have tended to be more efficient than governments at managing construction, service delivery, and asset maintenance (World Bank Group 2014). One frequently documented benefit among several Sub-Saharan African examples, where private management covers an estimated one-third of small piped water schemes, has been reduction of “non-revenue” water, or water losses for which production costs are never recovered. Among small-scale water providers in Uganda, a private sector participation model led to expanded coverage and financial performance with only modest tariff increases (World Bank Group 2014;Hirn 2013). Active connections tripled over 10 years with tariffs rising less than inflation.

In Madagascar, a host of rural community water user committees and private water operators have signed long-term concession agreements in which a private company invests in the water system to increase household access, generate more revenue, and share profits. This model has been replicated over roughly 15 years with donor support, such as USAID’s Rural Access to New Opportunities in Water, Sanitation, and Hygiene (RANO WASH) activity (Tetra Tech 2021).

Another long-running example of blended finance comes from Benin. Between 2007 and 2017, more than half of Benin’s rural piped water systems transitioned to private operation and maintenance contracts known as “affermages” (Comair, Delfieux, and Dakoure Sou 2021;Migan and Trémolet Consulting 2015). In these agreements, a private operator collects tariffs and then retains a percentage of an agreed-upon price per unit of water sold, turning over the remainder to the contracting authority (Janssens 2011). The initial pilot with 10 private operators successfully rehabilitated all water systems with no additional costs to the customers (World Bank Group 2018); however, subsequent scale-up experience brought a pivot to regional contracts to attract more professional operators. In 2022, a 10-year public-private partnership was formed with a consortium of French companies (Eranove, UDUMA, and Vergnet Hydro) to rehabilitate, extend, and operate rural water systems for 100% customer coverage (Marteau 2022). Public funds will ensure private connections and tariffs remain affordable.

Although some examples (e.g., Madagascar, Benin, Cambodia) have applied blended finance to rural water supply in low- and middle-income countries, it remains at a proof-of-concept stage. Blended finance is possible where rural water provision is more organized and mature and where people pay consistently, justifying lending. This is more likely to be the case in middle-income economies.

Further proof-of-concept is required to evaluate blended financing to drive rural water supply performance. It faces a dual challenge: persuading commercial lenders that water supply represents a lucrative investment opportunity and persuading water service providers to seek loans at rates higher than those routinely offered by development finance institutions.

Blended finance projects create an evidence base for effective public investment and in turn, incentivize the capture of better financial and impact data (Convergence 2019). Objective selection criteria may help “prime” service providers to continue the behaviors and actions that support blended finance (USAID 2022). Building the foundations for blended finance will require a transition period with accompanying public sector support, to allow for a paradigm shift on the part of both borrowers (who face increased pressure to manage operations efficiently) and lenders (who often do not know the market well enough to participate in investment opportunities).

While they take time, these adjustments have taken place in other sectors, most notably energy (IRC n.d.). Pories, Fonseca, and Delmon (2019) detail foundational issues ranging from governmental sector planning and tariff setting to service provider project preparation and financial market distortions. Experiences with the approach will elucidate the degree to which blended finance can work at large scales, but transformation is unlikely to occur rapidly.

Do you want to know more? Access to the complete report on financial innovations for rural water supply in low-resource settings HERE.

The information provided on this website is not official U.S. government information and does not represent the views or positions of the U.S. Agency for International Development or the U.S. Government.

This blog post is part of a series that summarizes the REAL-Water report, “Financial Innovations for Rural Water Supply in Low-Resource Settings,” which was developed by The Aquaya Institute and REAL-Water consortium members with support from the United States Agency for International Development (USAID). The report specifically focuses on identifying innovative financing mechanisms to tackle the significant challenge of providing safe and sustainable water supply in low-resource rural communities. These communities are characterized by smaller populations, dispersed settlements, and economic disadvantages, which create obstacles for cost recovery and hinder the realization of economies of scale.

Financial innovations have emerged as viable solutions to improve access to water supply services in low-resource settings. The REAL-Water report identifies seven financing or funding concepts that have the potential to address water supply challenges in rural communities:

Village Savings for Water

Digital Financial Services

Water Quality Assurance Funds

Performance-Based Funding

Development Impact Bonds

Standardized Life-Cycle Costing

Blending Public/Private Finance

Understanding Development Impact Bonds

One type of performance-based funding is a development impact bond (DIB), which involves involve a tripartite contract between a service provider, an impact/angel investor (seeking both financial and societal returns), and an outcome sponsor such as a development finance institution or government (Clarke, Chalkidou, and Nemzoff 2019). Moreover, DIB moves some risks from service providers and primary donors to a third-party investor, while rewarding water development outcomes.

For rural water particularly, bond investors would finance a program aimed at achieving a particular outcome or set of outcomes (e.g., extending household water connections), while service providers (e.g., public utility, private company, nongovernmental organization, or partnership) would be responsible for delivery. If and when the outcomes are verified by a third party, then the outcomes funder (e.g., government agency) should repay the social investor. In general, more successful programs give higher returns to investors.

The rationale for involving the impact investor as an intermediary is to plan the arrangement and provide the service provider with the capital required to execute planned activities (Center for Global Development and Social Finance Ltd 2013). DIBs enable development finance to retain a results-based structure without placing all of the risk on service providers themselves; rather, some risk is shifted to the impact investor (USAID and Palladium 2018). Minimizing overall risk requires careful program design, detailed costing of capital requirements and intended outcomes, and selection of a proficient service provider with a good track record of results.

As of 2018, seven DIBs have focused on improving agricultural, education, employment, and health outcomes for people and communities, with nearly $55 million set aside for project outcome payments. If outcome targets are achieved, private investors receive all of their upfront investment back; if the service provider achieves outcomes above prespecified target levels, investors receive interest (up to 7–15%); or, they may lose money if outcomes are not achieved. DIB case studies confirm design challenges (Belt, Kuleshov, and Minneboo 2017; Oroxom 2018; Convergence, Palladum, and Bartha Centre 2018; Kitzmuller et al. 2018). In particular, managing stakeholders’ different perspectives and priorities on funding and contract structures has proven difficult (Clarke, Chalkidou, and Nemzoff 2019).

A pioneering sanitation DIB used in Cambodia offers lessons on the benefits and challenges specific to WASH services (iDE 2022).

As shown in Figure 11, the institutions involved include:

1. USAID as the outcome funder;

2. The Stone Family Foundation as the impact investor; and

3. iDE as the service provider (an international nongovernmental organization that has operated in Cambodia for many years, facilitating uptake of sanitation services in rural areas).

Figure 2: Cambodia sanitation development impact bond structure (Adapted from iDE 2022)

The Cambodian DIB launched in 2019 and will run through 2023, with a maximum of $9.99 million in outcome-based payments from USAID back to the Stone Family Foundation (iDE 2022). The DIB aims to improve rural community sanitation services, especially for the poor and hard-to-reach groups (e.g., women, children, people with disabilities, and older people) across six provinces in Cambodia. Specifically, villages must achieve open-defecation-free status, as a

means of reducing disease burdens and preventing drinking water contamination. Outcome payments can be claimed in tranches (every 6 months) dependent on local village government reports collated and submitted by iDE. To mitigate risks, the financing structure relies on a

detailed operational model embedding the cost of services (plus risk premiums). This exercise envelops not just “core” activities but also a number of “soft” (i.e., enabling or supporting) activities. Activities in the latter category include capacity building, communications, engagement

with local authorities, and sourcing materials.

After the first 18 months, the program had enabled 750 villages (out of the targeted 1,600) to be declared free of open defecation (Morse 2021). From the service provider’s perspective (iDE), the DIB provides implementation flexibility and removes some of the project governance, design, and management burden, thus conserving costs. This flexibility is particularly important given the focus on harder-to-reach villages, which benefit from testing and innovative approaches that can be fine-tuned as the program rolls out.

Scale of dissemination

No DIBs have yet been trialed for rural water services in low- and middle-income countries. Given varied values and structural limitations of water development finance institutions, they may not hold universal appeal. One (in progress) seeks to address sanitation in Cambodia.

To access further information on financial innovations for rural water supply in low-resource settings, you can download the complete report HERE.

The information provided on this website is not official U.S. government information and does not represent the views or positions of the U.S. Agency for International Development or the U.S. Government.

This blog post is part of a series that summarizes the REAL-Water report, “Financial Innovations for Rural Water Supply in Low-Resource Settings,” which was developed by The Aquaya Institute and REAL-Water consortium members with support from the United States Agency for International Development (USAID). The report specifically focuses on identifying innovative financing mechanisms to tackle the significant challenge of providing safe and sustainable water supply in low-resource rural communities. These communities are characterized by smaller populations, dispersed settlements, and economic disadvantages, which create obstacles for cost recovery and hinder the realization of economies of scale.

Financial innovations have emerged as viable solutions to improve access to water supply services in low-resource settings. The REAL-Water report identifies seven financing or funding concepts that have the potential to address water supply challenges in rural communities:

Village Savings for Water

Digital Financial Services

Water Quality Assurance Funds

Performance-Based Funding

Development Impact Bonds

Standardized Life-Cycle Costing

Blending Public/Private Finance

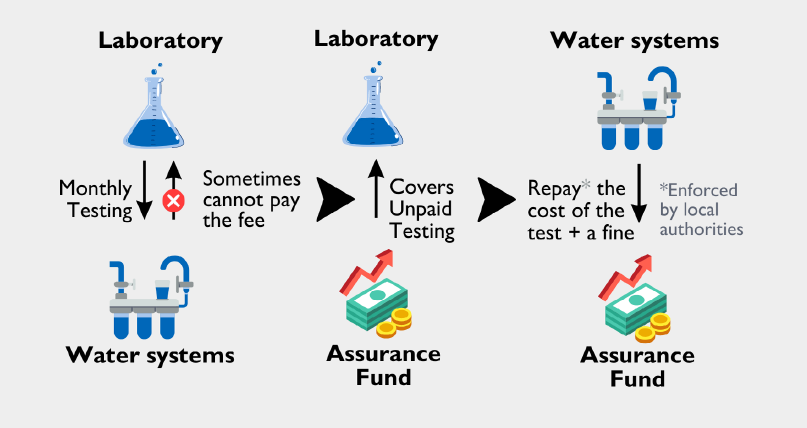

Understanding Water Quality Assurance Funds

In rural areas, community-managed water supplies are increasingly recognized as unsustainable, in part because communities with small water systems (e.g., handpumps, mechanized boreholes, and small piped systems) often struggle to collect enough money to maintain water infrastructure (Whaley et al. 2019). As a result, they typically must neglect critical aspects of professional water management, such as water quality testing to verify its safety for human consumption. Rural agricultural communities, situated far from public or private laboratories, struggle to access testing services due to distance and irregular income patterns. However, a viable solution comes in the form of introducing a third-party guarantor to distribute the risks associated with unpaid water testing fees among various stakeholders (Halvorson-Quevedo and Mirabile 2014). The third party can help to facilitate testing arrangements and provide indirect financial support, wherein stand-by funds are only accessed when the local fee-for-service exchange is disrupted.

How does it work?

“Assurance funds” provide liquid assets (e.g., a savings account) that can be quickly mobilized if a liability arises. Water quality assurance funds are held by a third party (e.g., a nongovernmental organization) to guarantee payment for to the beneficiary (e.g., a centrally located water quality laboratory) if a rural community is unable to pay for water testing services on time (Press-Williams et al. 2021).

By employing this innovative model, larger professional laboratories can extend low-cost centralized monitoring services to smaller rural water systems, fostering efficiency and incentivizing wider-scale testing. As a result, laboratories gain a new market for their services while rural communities gain a reliable means of verifying their drinking water safety with greater certainty and lower startup cost than establishing onsite laboratory capacity.The assurance fund accounting is managed by the third party and can be drawn down

slowly, leveraging donor aid, or replenished if the rural community is able to pay back service fees at a later date (Figure 1). Contract enforcement is managed through the local government authorities.

Figure 1. Simplified illustration of a water quality assurance fund mechanism (Source: Vanessa Guenther, The Aquaya Institute)

Implementation of assurance funds requires diligent management to ensure accountability. Skilled staff must manage the fund as long as it exists.For water quality assurance funds, field and laboratory staff must adhere to good protocols to ensure water quality data are accurate and address decision-making needs in a timely manner.

Examples

Pilot examples come from a few African countries:

With funding support from the Hilton Foundation, The Aquaya Institute (a nonprofit research and consulting organization) developed an assurance fund in 2020 to encourage an existing laboratory to provide water quality monitoring services to small rural water systems in the Asutifi North District of Ghana (Figure 2; Press-Williams et al. 2021). The water systems mobilized community-collected water fees to pay Ghana Water Company Limited’s (GWCL’s) central laboratory (Figure 3) for monthly services. If they defaulted on payments, then GWCL could file a claim against the assurance fund. This centralized testing approach cost an average of $67 per test, or approximately 60% of what it would have cost to provide training and testing equipment for each separate water system.

Between March 2020 and January 2021, GWCL testing revealed microbial contamination in more than half of the 134 water samples across nine water systems, raising awareness among water system managers about issues with chlorination procedures (Press-Williams et al. 2021). In most cases, water systems were able to pay GWCL within one month of receiving testing services. Despite payments being delayed for approximately one third of testing services, GWCL filed only one claim against the assurance fund, instead negotiating directly with the defaulting water systems to allow more time. Extension of the same concept to other districts in

Ghana as well as in Kenya, Uganda, and Tanzania is underway with additional funding support from USAID REAL Water, the Hilton Foundation, and the Helmsley Charitable Trust. Another use of the assurance fund was to deliver targeted subsidies for specific communities during times of need (e.g., Covid-19 pandemic, fuel price inflation).

Figure 2. Ghana Water Company Limited analyzes bacteria in drinking water samples from small water systems in the nearby rural district of Asutifi North. (Source: Bashiru Yachori, Aquaya Institute).

Figure 3. A Ghana Water Company Limited technician collects a sample from a water point in Asutifi North, Ghana, as part of the Water Quality Assurance Fund agreement (Source: Bashiru Yachori, Aquaya Institute).

To access further information on financial innovations for rural water supply in low-resource settings, you can download the complete report HERE.

The information provided on this website is not official U.S. government information and does not represent the views or positions of the U.S. Agency for International Development or the U.S. Government.

This blog post is part of a series that summarizes the REAL-Water report, “Financial Innovations for Rural Water Supply in Low-Resource Settings,” which was developed by The Aquaya Institute and REAL-Water consortium members with support from the United States Agency for International Development (USAID). The report specifically focuses on identifying innovative financing mechanisms to tackle the significant challenge of providing safe and sustainable water supply in low-resource rural communities. These communities are characterized by smaller populations, dispersed settlements, and economic disadvantages, which create obstacles to cost recovery and hinder the realization of economies of scale.

Financial innovations have emerged as viable solutions to improve access to water supply services in low-resource settings. The REAL-Water report identifies seven financing or funding concepts that have the potential to address water supply challenges in rural communities:

Village Savings for Water

Digital Financial Services

Water Quality Assurance Funds

Performance-Based Funding

Development Impact Bonds

Standardized Life-Cycle Costing

Blending Public/Private Finance

Understanding Digital financial services

Digital financial services have penetrated many aspects of daily life, including water services.

One strategy to address the gap in rural water funding is to increase the financial sustainability of water systems through improved water revenue collection and management (Waldron and Sotiriou 2017). In low-income countries, the collection of service fees primarily relies on cash, which can be labor-intensive, difficult to track, prone to miscalculations, and susceptible to theft or loss (Sharma, 2019). However, by implementing automated digital recording of time-stamped water usage and payment data, the planning, projection, and delivery of water services can be significantly improved (Waldron et al., 2019).Good record-keeping aids water service providers in tracking performance changes over time, as well as supporting financial sustainability, water conservation, and climate adaptation.

How does it work?

“Digital financial services” encompasses two concepts: financial services (e.g., payments,

savings, credit, insurance, user suport) and the technologies that deliver them to end users (Waldron et al. 2019). Services such as online savings or credit accounts mainly benefit adults who work outside the home and have bank accounts (Coulibaly 2021). The digital technologies accessible to users who rely on cash may include mobile money (electronic wallets using a mobile phone), water sale kiosks or “ATMs,” and prepaid token technologies (REAL-Water 2022).

Customers can use digital mechanisms to conveniently purchase water, reducing waiting times and operational downtimes when live vendors or caretakers are unavailable (Waldron et al., 2019). With prepaid digital services, the efficiency of water fee collection can reach nearly 100% (with the exception of targeted subsidies or discounts). “Postpaid” digital financial services, which collect fees retrospectively for prior water usage, enable service providers to automatically track outstanding payments and initiate billing. Digitization may enable better payment compliance, as those with seasonal or inconsistent income are able to deposit a sum of money and draw on it over time (Sharma 2019).

Moreover, the implementation of prepaid metering for automated water dispensing devices and postpaid digital water service accounting brings benefits to both water system operators and customers, improving fee collection consistency as well as convenience. They may likewise simplify subsidy delivery to vulnerable customer segments.

Figure 1. Training a customer in Ruiru, Kenya on how to use his phone for making

water payments (Source: Joyce Kisiangani, The Aquaya Institute)

Examples

Technology provider Grundfos partnered with the nongovernmental organization World Vision and Safaricom, the leading telecommunications provider in Kenya, to install 32 self-service water kiosks (called LifeLink systems) in locations that lacked water infrastructure, serving both

homes and businesses (Waldron et al. 2019). Initial uptake was high and interviews documented user benefits from reduced favoritism in water distribution as well as being able to track and review spending. Collecting mobile payments cost less than collecting cash payments, a savings that could be reinvested to upgrade services or passed onto consumers (Sharma 2019). The World Bank and others have likewise been working to scale affordable water installations in Tanzania using prepaid Grundfos card kiosks combined with solar pumping, which vastly reduces water transportation time and stabilizes high prices offered by private sellers (World Bank 2017). Recognized downsides of this and other digital payment examples have included questions of who requires data access, remote monitoring needs, labor cuts, reduced customer service capabilities, and difficulty paying among the ultra-poor (Waldron et al. 2019).

The nonprofit organization Safe Water Network uses Hangzhou LAISON Technology digital household prepaid meters in their piped connection program in Ghana. Customers receive a device to input a token purchased through mobile money. New users joined quickly following customer workshops to explain the payment system, and the enhanced cost recovery shifted the operation from a net loss to a net surplus (Waldron et al. 2019). Ensuring proper use will likely require sustained engagement. Safe Water Network has continued expanding the household connection metering program to serve several thousand households in small rural towns in Ghana’s Ashanti Region.

Transitioning to digital payments comes with certain challenges, such as additional transaction fees, costly startup infrastructure, poor telecommunications technology, skepticism towards technology, and the belief that water services should be cheaper or free, as well as income loss for traditional vendors who primarily handle cash transactions. Local training support and outreach efforts for social inclusion can be beneficial for expanding digital services. However, digital financial services do not represent a fix-all solution. Their successful implementation requires substantial training and effective governance to transition service providers and communities to new processes that increase collection efficiency, while minimizing the impact on customers’ water usage (Heymans, Eales, and Franceys, 2014).

Digital financial service innovations have made inroads globally in urban areas and are rapidly expanding to serve rural residents in Africa, Asia, and Latin America. As use expands, social inclusion efforts may be needed to ensure the services benefit vulnerable populations (Coulibaly 2021).

To access further information on financial innovations for rural water supply in low-resource settings, you can download the complete report HERE.

The information provided on this website is not official U.S. government information and does not represent the views or positions of the U.S. Agency for International Development or the U.S. Government.

This blog post is part of a series that summarizes the REAL-Water report, “Financial Innovations for Rural Water Supply in Low-Resource Settings,” which was developed by The Aquaya Institute and REAL-Water consortium members with support from the United States Agency for International Development (USAID). The report specifically focuses on identifying innovative financing mechanisms to tackle the significant challenge of providing safe and sustainable water supply in low-resource rural communities. These communities are characterized by smaller populations, dispersed settlements, and economic disadvantages, which create obstacles for cost recovery and hinder the realization of economies of scale.

Financial innovations have emerged as viable solutions to improve access to water supply services in low-resource settings. The REAL-Water report identifies seven financing or funding concepts that have the potential to address water supply challenges in rural communities:

Village Savings for Water

Digital Financial Services

Water Quality Assurance Funds

Performance-Based Funding

Development Impact Bonds

Standardized Life-Cycle Costing

Blending Public/Private Finance

Understanding Village Savings for Water

Community-based savings and credit associations offer rural dwellers in low-income settings an opportunity for member-only access to loans, emergency support, and small annual investment returns. With abundant existing savings groups in sub-Saharan Africa and India, the mechanism has been leveraged in some cases to improve financial management of rural water systems. They offer a framework for creating dedicated, affordable, and transparent savings funds to pay for high-quality maintenance and repairs. Groups may dissolve over time, though, and require periodic external support. Field results from limited-scale water initiatives in several African countries have maintained an above-average reserve fund to support water point maintenance, repairs, or upgrades (The Water Trust 2022).

How does it work?

One low-barrier approach to improve funding for water system maintenance shifts financial management duties from volunteer water committees to new or existing community-based savings and credit associations. These self-selected, self-governed groups offer rural residents informal yet structured financial services with several built-in accountability mechanisms. Groups made up of 5–40 members usually operate on a 12-month cycle (VSL Associates 2022; Orr et al. 2019; Allen and Panetta 2010; Swinderen et al. 2020). At the beginning of each cycle, the group develops a constitution, defining savings and borrowing terms along with group bylaws (Figure 1). At weekly or monthly meetings, each member deposits the agreed amount of money into a common fund. Members can then take small, low-interest loans from this internally-generated capital. At the end of the cycle, each member receives their savings plus a portion of the overall interest earned from loans. Many savings groups offer a small mutual insurance scheme as well, using funds to provide allowances or no-interest loans in the case of unexpected member hardships (e.g., family illness or death).

Figure 1. Typical community savings group approach (Source: Vanessa Guenther, The Aquaya Institute)

The saving group model offers several advantages, including transparency, accountability, and trust-building among members. Successful implementation examples in sub-Saharan Africa, particularly in Uganda, have demonstrated their positive impact on water point management. By integrating savings groups, water user committees have reinforced accountability and improved the community’s commitment to paying for water services.

However, this model also faces challenges, such as limited capacity and technical expertise, the potential disintegration of savings groups, and the need for ongoing subsidization of maintenance services. While there may be initial costs associated with establishing savings groups, the return on investment can be significant. For instance, external support costs for savings group startup could exceed $1,000 per system, with a longer time frame needed to observe returns in the form of a sustained water fund (The Aquaya Institute, in press); however, the return on investment considering all-purpose savings can reach up to 20:1 (Krause 2022).

Examples

In sub-Saharan Africa, savings groups have been utilized to support water point management. In the Lira district of Northern Uganda, existing water user committees began offering small loans for personal needs, which reinforced their record-keeping accountability as well as the community’s commitment to paying monthly for water services (Nabunnya et al. 2012). Challenges included some refusal to pay for water and the informal process and money handling approach (by the local volunteer treasurer). In the Kamwenge district of southwestern Uganda, Water for People trained communities on financial planning for water point breakdowns, with savings groups as one of the strategy options (Muhangi 2018). Additional Ugandan examples come from Link to Progress (Piracel 2021), The Aquaya Institute (Marshall, Guenther, and Delaire 2021), WE Consult and Charity Water, Lifewater International, and Amref (Teo 2016). SEND has supported savings groups in Sierra Leone (SEND 2020), while the USAID West Africa Water, Sanitation, and Hygiene Program (USAID ND) and the nongovernmental organization WaSaDev have supported savings groups in Ghana.

In Malawian “borehole banking,” a central account is established at a water point and contributions are made through monthly water user fees. Then, community members who contribute can access loans, to be paid back with interest to the water point account (Mbewe 2018).

A pilot of 175 water points with “borehole banks” achieved an average savings of approximately $80 for operation and maintenance, about ten times higher than the average savings reported for water points without borehole banks. The rate of functionality increased from 64% to 94% between 2015 and 2017.

In another program from Uganda, The Water Trust worked with VSLAs to set aside an agreed-upon fraction of members’ payments earmarked as a “water point reserve fund,” which can only be used for handpump maintenance. Monitoring results have been encouraging: in the 2017 pilot, 32 water points with VSLA-based water funds had collected an annual average fund about four times greater than 28 communities relying on coached water user committees or a maintenance contract approach alone (Prottas, Dioguardi, and Aguti 2018). By 2020, The Water Trust invested training resources to extend the approach to more than 200 communities, with annual reserve funds continuing to meet or exceed target amounts (The Water Trust 2020). The approach has expanded to cover more than 700 water points, documenting higher measures of water point functionality and active water point management for water points with an associated VSLA (The Water Trust 2022).

Figure 2. Village Savings and Loan Association members in the Kabarole district, Uganda, holding up their passbooks (Source: Katherine Marshall, The Aquaya Institute)

Although the concept of using savings groups to mobilize and manage water point funds has existed for several years (Agbenorheri and Fonseca 2005), this approach is not yet common and remains in the early stages of evaluation research (e.g., by The Water Trust and The Aquaya Institute). Despite compelling examples, its application to serve rural water supply services is globally limited. The knowledge base comes almost exclusively from implementation experience, with fewer examples of rigorous evaluation at scale. Improved documentation would improve the sector’s understanding of how to most effectively leverage community savings groups to improve rural water services.

Savings groups supporting water point management are of interest to government service providers and NGOs offering subsidies. Rural service providers facing challenges with inconsistent user payments should consider experimenting with community savings groups, particularly in areas where pay-as-you-fetch systems are underperforming, such as communities served by public handpumps (Marshall, Guenther, and Delaire 2021). Danert (2022) estimates that approximately 20% (ranging from 1%–60%, by country) of sub-Saharan

Africa’s population relies on handpumps. Additional opportunities arise in communities with gravity flow schemes and mechanized boreholes that have regularly struggled to collect revenue.

To access further information on financial innovations for rural water supply in low-resource settings, you can download the complete report HERE.

The information provided on this website is not official U.S. government information and does not represent the views or positions of the U.S. Agency for International Development or the U.S. Government.

A sum of money granted by the state or a public body to help an industry or business keep the price of a commodity or service low

— Oxford English Dictionary

Rural Water Services ARE Subsidized

Even the United States has subsidies for rural water services. This doesn’t make something unsustainable. However, it does create a critical need for clarity of the total cost of the services, how it is funded, and how it will continue to be funded. There also needs to be a good definition of what the costs are (CapEx vs OpEx vs CapManEx). Thankfully our friends at IRC have laid this out here.

The challenge of achieving the SDGs is upon us and with this concrete and short-term objective, the sector is finally taking the issue of financing more seriously, which is a very good thing but not before time. Whilst a few years ago finance was the privilege of a selected few, everyone is now talking about it; however, whether this is a case of better late than never still needs to be proven.

The challenge of achieving the SDGs is upon us and with this concrete and short-term objective, the sector is finally taking the issue of financing more seriously, which is a very good thing but not before time. Whilst a few years ago finance was the privilege of a selected few, everyone is now talking about it; however, whether this is a case of better late than never still needs to be proven.

Last week, I chaired with interest the RWSN webinars on “grown up finance” for rural water supply. Kelly-Ann Naylor (UNICEF), Catarina Fonseca (IRC WASH), Sophie Trémolet and John Ikeda (World Bank) and Johanna Koehler (Oxford University) gave great presentations and here are my few take aways from the discussions:

The magnitude of the challenge is huge and greater than we probably think. We often hear about the figure of USD 114 billion to achieve SDGs 6.1 and 6.2, but this is only part of the story. This figure covers investment and maintenance of new services, but excludes the crucial maintenance of existing services and the broader sector support.

We know there is a huge funding gap and the current finance model will not fit the bill. Official Development Assistance (ODA) has not increased as much for WASH as it has for other sectors and concessional finance as well as domestic investments only accounts for a fraction of the required investments. The sector has the potential to attract other sources of finance, but we need to take a few steps.

We need to have an honest conversation about the exact magnitude of the challenge at national and district level to support planning and budgeting. This is taking place at national level as part of the SWA process in some countries, but only partially at district level. More robust data on service levels as well as cost of services, which are currently insufficiently researched, can help us in this direction, but we need to move faster.

We need to get better at understanding budgeting processes and supporting strategic multi-year budgeting both at national and district levels. Most countries are not very good at this at the moment and it has to change.

We need to advocate beyond the WASH sector and target more important political decision makers – Ministries of Finance and even the office of the president) to prioritise domestic investment in WASH and increase it through a larger tax base and increasing tariffs. Again, evidence will take us a long way in bringing politicians round the table.

We need to look at other sources of finance, particularly private finance to complement existing funding sources. Making the sector more attractive to private investment will be a necessary first step, but this will hinge on Governments playing a crucial role in strengthening the enabling environment and de-risking the sector. ODA, currently crowding the sector will need to focus on the riskiest segments and leave space for private investments to come in (e.g. stop lending to urban utilities and focus on rural water supply). Assessing sector entities’ performance and risk profile will be a necessary first step.

We need to start experimenting with innovative “blended finance” models, learn from them and adjust. Examples are already out there from Benin, where subsidised concessions are being tested; but also from Kenya and other countries.

After decades of ODA dependency, the WASH sector is slowly opening up to the real world of finance to reach its ambitious targets. This means being transparent and accountable, providing evidence of performance and better understanding what will incentivize the commercial finance world. A huge task ahead and surely a dramatic and positive change in culture!

Photo: Inspecting community-level financial records in Tajikistan (S. Furey)